This year’s Quids in! Cost of Living Survey paints a stark picture of the challenges facing lower-income households.

Almost 1,100 social tenants and low-income earners responded to the Quids in! Cost of Living Survey, and their feedback reveals how deeply the current crisis is biting.

It tells a story. One we all recognise, but now with data to back it up. One that we need the government to listen to.

The Evidence: Lives on the Edge

It’s no secret that millions are struggling, but the survey details exactly how:

- Skipping Basics: Over a third (34.1%) of respondents skip meals to save money. Two in five (40.5%) are living without heat, even when it’s cold.

- Financial Anxiety: 40.6% feel scared, worried, or sad about money. One in five (22%) say stress has made them physically ill, and almost 15% have fallen behind on rent.

- Coping Mechanisms: 19.3% have used a food bank. One in five (19.4%) have switched back to cash to manage spending. Around 44.8% have cut back on social events, with nearly one in ten (9.2%) cancelling home contents insurance.

None of this is new to support workers, housing officers, and local councillors on the front line. The data is evidence that the cost-of-living crisis remains at critical levels. And there’s more devil with more detail.

Vulnerable Groups in Focus

The survey also highlights which groups are feeling the brunt.

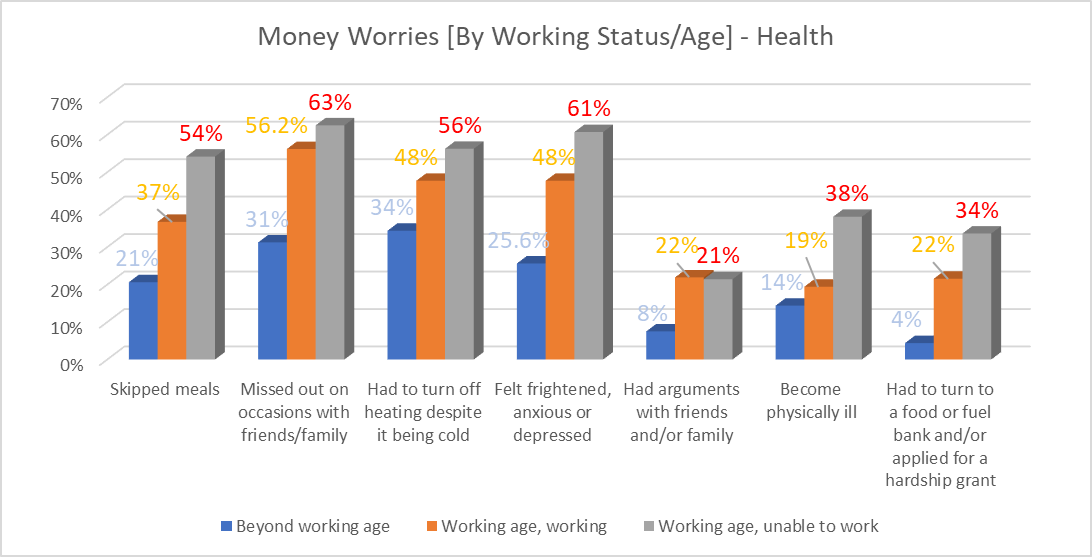

- Those Unable to Work

- Over half (54%) skip meals.

- 56% turn off the heating.

- 61% are anxious about money, and 38% say that stress has directly affected their health.

- 21% are in rent arrears.

- Working Households

- 37% skip meals, 48% go cold.

- One in five (22%) have used a food bank.

- 15% report “big money problems,” with 20% in rent arrears.

- Older People

- Generally better off: Only 4% in rent debt versus around 20% for working-age respondents.

- But still a third (34%) go cold, one in five (21%) skip meals, and 26% feel anxious about money.

For those of us delivering frontline services, these figures confirm that no demographic is untouched. Older people report fewer problems, but they’re not insignificant. It’s just that they’re much, much worse for working age people who are unable to work, as the chart above shows.

A notable trend is the shift back to cash-based budgeting, across all groups. A quarter (25%) say they have moved to cash as a response to financial worries. For some, physical money makes it easier to stay on top of outgoings when every pound counts. However, as retailers and transport go cashless, the risk is that those most in need of tight budgeting tools get left behind by a digital-only marketplace.

Feeling Quids in!

It’s encouraging to see that more than half (53%) of people who receive Quids in! resources find them helpful “all the time” or “often.” A further 38% find them “often” useful, and 20% have taken direct action based on our advice.

This includes printed guides and licensed email content shared by landlords to their tenants. Crucially, 36% say these help them feel less alone. That sense of community is vital, especially as many feel the system isn’t listening to them.

Our published promise to people in hardship is: We see you. We hear you. We are you. The survey is one way to listen and to amplify their voice. We know professionals and policymakers rely on data and best-practice guidance. That’s why we share these findings—not just to illuminate the crisis, but to inform real solutions.

Sector Responses

While government-level changes are critical, there’s also much we can do at a local and organisational level:

- Targeted Outreach

- For those at risk of falling behind on rent, early intervention can make a world of difference, initiating support before arrears become debt crisis.

- Housing teams and health services can collaborate to tackle financial and health problems together, while working with independent income maximisation initiatives (like Quids in!) can add value.

- Whenever possible, promote urgent action people can take for themselves, sharing guidance and advertising the gains to be had. Work with trusted third parties, wherever it can make the difference.

- Cash-Friendly Services

- Ensure your payment points still accept cash.

- Provide guidance on how to transition between digital and cash budgeting, so people can choose what works best for them.

- Facilitate local partnerships, like with credit unions and community support agencies, to create a safety net for residents at greatest risk.

- Invest in the experts – people with lived experience themselves. The best thing Quids in! ever did was build peer work into its community support programmes, now the majority of our staff speak with authenticity and empathy when providing money guidance.

- Benefits Advice & Income Maximisation

- Focus on prevention by looking at best practice for boosting take-up of entitlements, particularly health-related benefits.

- Think beyond benefits too – employment, however modest the earnings are to start, is too often treated as the cherry on the cake. It brings more than money to working households.

- Train staff to recognise the signs of severe financial stress and signpost to services like debt counselling, welfare rights, or food banks.

- Advocacy with Government

- Use data (like Quids in! survey findings) to lobby MPs, councillors, and policymakers for increased investment in health, welfare, and housing.

- Highlight where policy decisions (such as means-testing Winter Fuel Payments) might inadvertently harm certain groups.

Professional Development

In April, the Quids in! Professional Network will host a webinar to dive deeper into these results. We’ll match the experiences of people who seldom get a voice against government priorities, and work together to identify practical interventions.

Our webinars are an opportunity for housing providers, local authorities, policy advisers, and frontline workers to deep dive into subjects and collaborate on making meaningful change. Our next event is on debt support (24th February), then in March we’re staging two: One looks at the future of digital comms (6th March) and the other explores ways to increase consumer power to exercise their rights (17th March). [Full details of all events here.]

The Cost of Living Survey 2024/25 confirms we’re still in the thick of things. As professionals on the frontline, we also have a responsibility to challenge, innovate, and advocate. By coming together, sharing insights, and pushing for reforms, we can ensure that the voices behind these alarming figures do not go unheard.

Image: Dmitry Demidovich / Shutterstock